This post was also published today in Forbes.

Startup investing is a funny thing. Sometimes it feels like you are on fire. You see exciting companies and founders coming one right after another. Other times, nothing coming through the pipeline feels quite right, no matter how many you are seeing. After experiencing several of these hot and cold cycles, I was curious how normal this is. I decided to take a look.

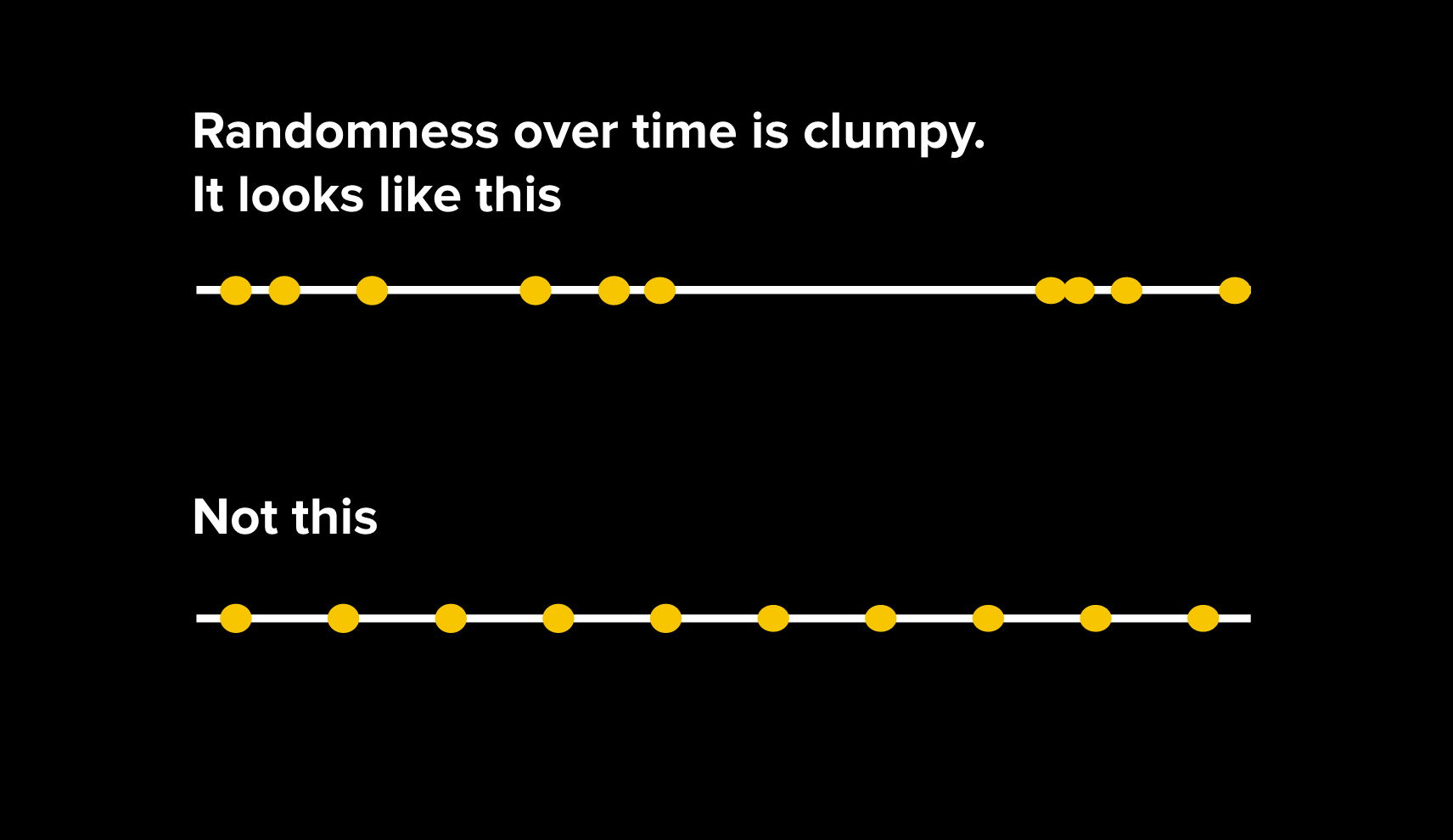

Let’s begin with an idea that many investors strive for: investing at a steady pace. Simple, right? Investing at a steady pace sounds intuitive enough. The only problem is that it's a bad idea.

The reality is that the best opportunities are not evenly distributed over time. Randomness is clumpy. If you invest in only the best opportunities, whenever they arise, you will have busy and slow periods. Smart investing plans for the clustering.

Randomness means clumping.

Consider the math. I randomized 10,000 scenarios to understand how the ten best investments I see every year will be distributed over that time. The math is a poisson process. The results are interesting for any investor. If you want to run your own scenarios, feel free to use the basic model I built here.

I target ten investments a year. You might think that I would aim for 2-3 investments per quarter. But actually, the randomized scenarios make it clear that a “normal” quarter only happens half of the time. I am just as likely to have a sleeper quarter (0-1 deals) or a slammed quarter (4-6 deals).

A normal quarter only happens half the time.

A few other highlights from my analysis:

- In 3 out of 4 years, there will be one sleeper and one slammed quarter—big ebbs and flows are the norms. You should plan on this, not on steady investing over a year or a fund's life

- In 1 out of 3 years, half or more of the best opportunities will come in a single quarter

- In 1 out of 4 years, you will have a quarter with zero opportunities

The lesson is clear: investors who try to invest at a steady pace will not be investing in the best opportunities. To only invest in the best companies, you need a flexible investing calendar.

This math assumes that the best deals are randomly distributed throughout the year. If you believe that there is seasonality driven by accelerators, school graduations, or founders quitting jobs at the end-of-year, then the opportunities will be even more clustered.

I struggle with this myself sometimes. Recently, I had made two back-to-back investments when a third exciting startup also caught my attention. At the time, I questioned whether I was being too eager, perhaps having too optimistic an outlook that month. The reality, though, is that opportunities very often cluster, and I did make that third bet—a clear win in hindsight.

There are of course some advantages to investing at a steady pace. Remaining active in the market keeps your networks active, your brand fresh, and your knowledge relevant. It simplifies planning for a fund's manager and limited partners. And it prevents you from letting good opportunities pass you by, waiting for a perfect deal that doesn't exist. Venture will always be about taking risks and putting your neck out there.

So, how do you know when to bet? The key is to find balance.

The wrong approach is to hold yourself and your team to strict investment quotas per quarter or year. A better approach is to set a range that incorporates the natural ebbs and flows of randomness, and to discuss expectations with your team and limited partners. Running scenarios against your portfolio size and investment period will help you understand the clumpiness expected in your own model.

Understanding the randomness of opportunities will help you plan smarter. Steady investing, rather than pursuing the best companies when they actually are ready for investments, will ensure sub-par investing and returns. It will cause you to miss out on excellent deals—don't make that mistake.